New York is one of the most complex medical liability environments in the country. The state’s mix of high patient volume, active plaintiff attorneys, and venue-driven severity makes it a place where coverage decisions carry real financial weight. Surgeons, procedural specialties, and doctors practicing in the New York City metro area feel this most, but every doctor in the state benefits from understanding how the market works.

This guide focuses on the essentials: how medical malpractice insurance coverage is structured in New York, what hospitals expect, how pricing works, and what doctors should know when evaluating options. The goal is simple - clear information that helps you make confident decisions without sifting through unnecessary detail.

New York’s liability landscape differs sharply from most states. Several factors shape the risk environment:

New York consistently reports some of the highest medical malpractice verdicts in the nation. The state does not cap economic or non-economic damages, which increases the potential severity of claims. This is especially relevant for surgeons, OB/GYNs, anesthesiologists, and specialists who manage high-acuity cases.

Where you practice influences everything from premium level to carrier appetite.

The same specialty can see stark differences in pricing just by crossing a county line.

New York has a dense and active plaintiff attorney presence. Attorneys regularly advertise for surgical claims, birth injury cases, and delayed-diagnosis matters. This shapes insurance carrier behavior and increases the importance of policy structure and limits.

While the state doesn’t legally mandate malpractice insurance, nearly every hospital and ASC does. Requirements vary by system, but commonly address: minimum limits, acceptable carriers, admitted status, additional insured provisions, and procedure-specific approvals.

Credentialing rules tend to be stricter in New York than in many states, which can influence which insurance companies are available to you.

New York’s longer statute of limitations and multi-year discovery timelines mean claims often emerge from care delivered two to three years prior. This increases the importance of clean retro dates, strong documentation, and smooth transitions when changing jobs.

New York doesn’t impose a statewide legal requirement for doctors to carry malpractice insurance, but in practice, nearly every doctor needs coverage to work inside a hospital or ASC. Credentialing committees, group contracts, and facility bylaws drive the standards here, not state statute.

Most physicians encounter similar expectations across the state, even though the risk varies dramatically between counties.

These requirements vary by system but generally include:

This applies consistently across major systems in NYC, Long Island, Westchester, and most upstate regions.

$1 Million / $3 Million

New York hospitals typically reference two structures:

Common across much of the state.

$1.3 Million / $3.9 Million

Frequently required in higher-severity regions, especially NYC metro and Long Island.

Surgical and high-acuity specialties may see additional expectations for excess layers depending on facility policy.

New York is unusual because both policy types are widely available.

Occurrence Coverage

Claims-Made Coverage

For foundational definitions, the National Association of Insurance Commissioners (NAIC) provides clear explanations.

You can also review our claims made vs occurrence guide.

Hospitals and groups may request:

These reviews are standard during credentialing, onboarding, and hospital privileging.

New York has one of the most diverse malpractice insurance marketplaces in the country. Physicians encounter admitted carriers, excess and surplus lines markets, risk retention groups, and a unique state-funded excess program. Each option serves a different purpose, and which one is appropriate depends heavily on specialty, procedure mix, prior acts history, and where you practice.

Admitted carriers are licensed by the New York State Department of Financial Services (DFS) and must follow state rules on rates, policy forms, and financial reserves. They also participate in the New York Property/Casualty Insurance Security Fund, which offers limited protection if a licensed insurer becomes insolvent.

Hospitals and ASCs across the state commonly prefer primary coverage from an admitted carrier. For many physicians - especially surgeons and high-risk procedural specialties - admitted policies form the foundation of their credentialing requirements.

E&S carriers (non-admitted insurers) operate outside DFS rate regulation and do not participate in the guaranty fund. That flexibility allows them to consider risk profiles that admitted carriers may decline.

Physicians often turn to E&S markets when they have prior claims, work in very high-exposure specialties, perform office-based procedures or sedation, or have non-traditional practice structures. E&S carriers also step in when admitted carriers cannot offer terms that fit the physician’s procedural work or underwriting profile.

The National Association of Insurance Commissioners (NAIC) provides a high-level explanation of how surplus lines markets function nationally, which helps put this segment of the market into context.

Risk Retention Groups (RRGs)

RRGs are liability insurers formed under the federal Liability Risk Retention Act (LRRA). They can insure physicians across state lines once registered in New York, but they are not admitted carriers and do not participate in the state guaranty fund.

LRRA statute (U.S. Government Publishing Office)

Hospital acceptance varies. Some systems permit RRG coverage; others expect physicians to use admitted carriers. For this reason, RRG participation is usually a credentialing discussion early in the process.

New York also offers a unique, state-funded excess layer commonly referred to as Section 18. This program provides an additional limit above a physician’s primary coverage and is especially relevant for surgeons practicing in high-severity venues.

Eligibility typically requires primary coverage with a New York-licensed admitted carrier, active privileges at a participating hospital, completion of risk-management coursework, and hospital selection for enrollment. Because funding is limited and allocated annually, participation isn’t guaranteed even when all criteria are met.

The regulatory framework is outlined in 11 NYCRR Part 152 for those who want a deeper look.

New York’s market allows for multiple coverage structures, depending on the physician’s circumstances: native graph?

The right fit depends on your specialty, county, case mix, and hospital relationships.

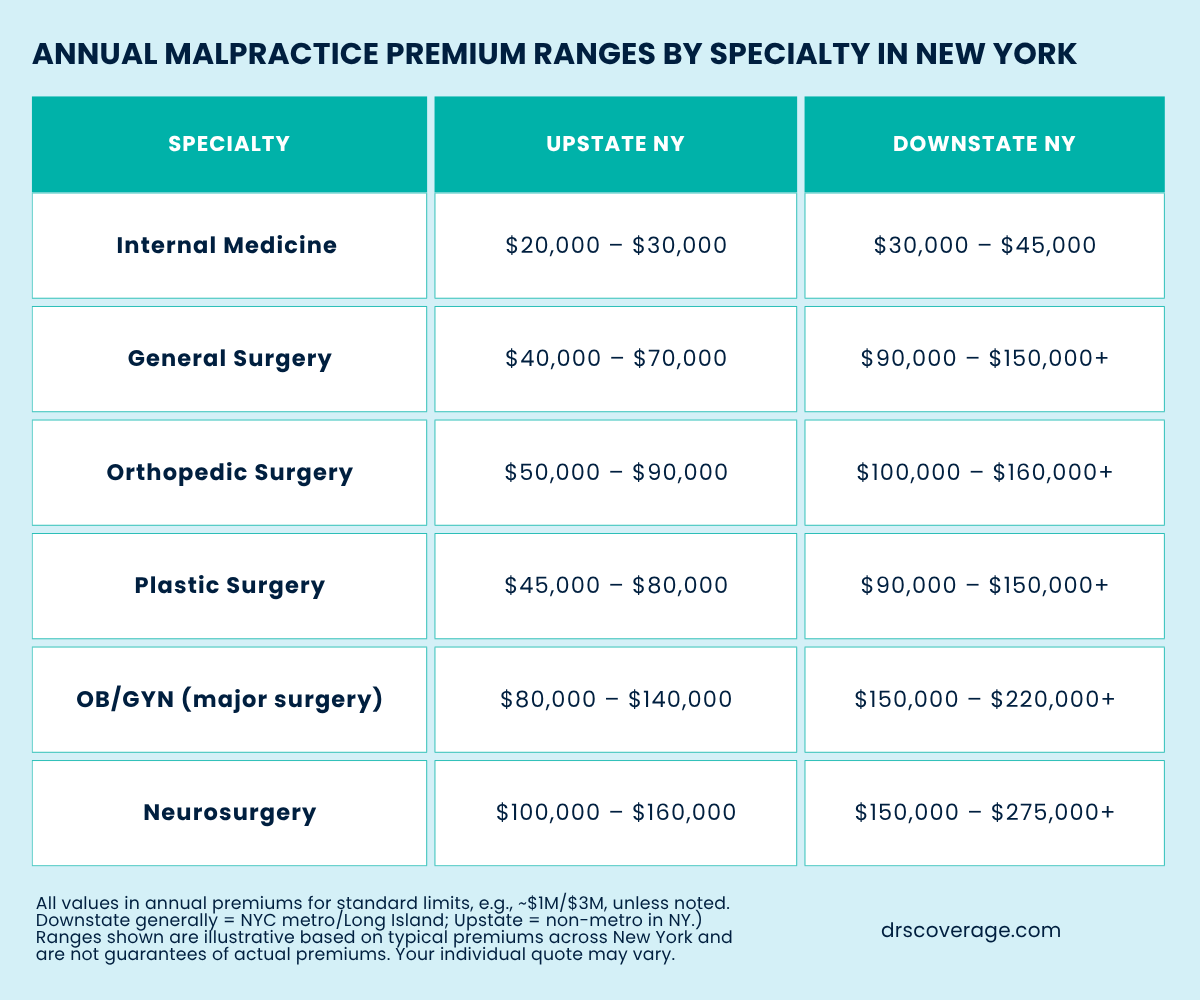

Malpractice premiums in New York vary more than in most states. The combination of venue severity, specialty exposure, and procedural complexity creates a wide pricing range. High-risk specialties practicing in New York City, Long Island, or Westchester typically see the highest premiums, while physicians upstate often pay far less for similar work.

Patterns tend to follow a predictable structure across the state:

A general surgeon in Manhattan may see pricing several times higher than a surgeon in Buffalo or Syracuse. The risk profile hasn’t changed - the venue has.

Several factors combine to shape the premium landscape. Understanding these helps physicians interpret renewal changes, evaluate job offers, or plan a move to another county.

County and Venue Severity

Where you practice matters as much as what you do.

New York’s verdict history is heavily concentrated in a handful of counties:

This is why two surgeons with identical training and case mix can have radically different premiums based on ZIP code.

Specialty is a major driver.

Carriers stratify specialties based on the potential severity of outcomes. Surgical fields tend to land in higher tiers, especially when cases involve: spine, neurosurgery, bariatric surgery, trauma, high-risk plastics, and OB-related surgical work.

Carriers also look closely at procedural detail: robotics, surgical volume, anesthesia type, inpatient vs ASC case mix, and complication rates.

New York carriers tend to weigh claims more heavily because the state allows longer discovery timelines. A past event may show up again during underwriting years later, especially if the claim involves complex documentation.

Even small or closed-without-payment matters can influence rating, depending on the carrier.

Carriers evaluate not just the specialty, but how the specialty is practiced:

These variables often move a physician into a different underwriting tier.

Pricing can also shift based on: solo practice, group practice, hospital employment, academic or hybrid models, shared vs individual limits, and entity coverage needs.

Credentialing requirements vary widely between systems, adding another layer of complexity for physicians who practice at multiple facilities.

Tail coverage becomes especially important in New York, where reporting timelines can stretch for years and claims often surface long after a physician has moved on from a role. Understanding when tail is required, when it isn’t, and how New York’s policy structure affects your options can save you a significant amount of stress during transitions.

This section covers the key scenarios physicians encounter across the state, including how occurrence policies fit into the picture and what retirement looks like under New York’s carrier landscape.

Tail insurance is required anytime a claims-made policy ends and you no longer have an active policy protecting past care. This includes:

A claim filed years later must attach back to your policy in place at the time of the care, which is why tail coverage fills the gap once a claims-made policy stops.

If you’re approaching a transition and want to review tail options, DrsCoverage can walk you through what’s available and provide tail quotes for your situation.

When Tail Coverage Is Not Needed: Occurrence Policies

New York is one of the few states where occurrence policies are still widely available, which gives physicians more flexibility than in many other markets.

An occurrence policy protects you based on when the care was delivered, not when the claim is reported. If the incident happened while the policy was active, it’s covered – even if the claim surfaces years later.

So thus, with an occurrence policy:

Because New York offers both claims-made and occurrence coverage, physicians can select the structure that fits their career path and risk profile. Availability depends on specialty and county.

Occurrence is common for primary care, pediatrics, internal medicine, and some surgical fields depending on the carrier. For higher-acuity specialties, eligibility varies based on case mix and procedural exposure.

Retirement tail in New York follows the same basic rules you’ll see nationally, but carrier requirements can differ across admitted, E&S, and RRG markets.

Most carriers provide no-cost retirement tail when a physician:

The last point surprises many physicians. Even a small amount of hands-on work – limited telemedicine, part-time weekend coverage, or occasional procedures – can disqualify you from receiving retirement tail.

Because each New York carrier handles retirement differently, it’s worth clarifying your eligibility before you actually step out of practice. This avoids last-minute surprises and makes planning easier.

New York’s legal environment influences nearly every part of the malpractice market - from underwriting and premiums to tail pricing and hospital credentialing. The state has no cap on non-economic damages, active plaintiff litigation in several downstate counties, and timing rules that can allow certain claims to surface years after the clinical event.

New York is one of the few high-severity states without tort reform limiting non-economic damages. Juries can award any amount for pain and suffering, subject only to judicial review. This contributes to:

New York’s statute of limitations for medical malpractice cases is generally 2 years and 6 months from the alleged negligent act. However, several rules can extend or shift this timeline:

These timing rules are part of why claims in New York can appear long after the initial incident - a factor carriers consider when pricing claims-made policies and tail.

These timelines are general summaries. Physicians should consult a qualified attorney for guidance on how New York’s statutes apply to a specific situation.

New York’s claims environment plays a major role in how carriers underwrite surgeons and other high-risk specialties. While the state is known for larger verdict potential in several counties, the overall picture is more nuanced. Most physicians are surprised by how differently claims unfold here compared to lower-severity states.

Despite New York’s reputation, the majority of malpractice claims do not result in an indemnity payment. Many cases center on communication issues, documentation questions, delayed diagnoses, or postoperative timelines. Even when a claim doesn’t settle, defense costs can be significant, and these expenses shape underwriting and rating structure.

Malpractice cases in New York often take longer to resolve due to:

These extended timelines affect how carriers price claims-made coverage, how reserves are managed, and how tail premiums are calculated.

In New York, documentation quality is often more influential than in many states because plaintiff attorneys leverage broader discovery and timeline arguments. Detailed charting, postoperative documentation, and communication records frequently shape how a claim develops - even when clinical care meets standard-of-care expectations.

When to Review Your Coverage in New York

Most physicians in New York only revisit their malpractice coverage when something forces the issue - a credentialing deadline, a contract change, or a move between systems. But a few common transitions tend to impact your policy more than doctors expect. These are the moments when taking a closer look is worth your time.

Different hospitals in New York prefer different carriers, limits, and retro date structures. A switch between NYC academic centers, large downstate systems, or independent upstate hospitals often means new credentialing requirements that affect your policy.

Premiums, carrier appetite, and underwriting shift dramatically depending on venue severity. A move from Rochester to Long Island, or vice-versa, usually changes pricing and sometimes determines whether you stay with an admitted carrier or need an E&S option.

Adding higher-exposure cases (OB, trauma call, complex plastics, neuro, or orthopedic procedures) or scaling them back can move you into a different underwriting category. Even subtle changes - like adding sedation or increasing surgical volume - can impact pricing.

Employment contracts often determine:

A quick review before you sign can prevent surprises later.

Some NY carriers offer reduced rates for lower clinical volume or part-time schedules, but the structure varies. It’s worth checking how your current practice level fits into your policy.

If you’re approaching retirement age or stepping away temporarily, your tail options shift. Some carriers offer free retirement tail under specific conditions; others don’t. Planning ahead makes the transition much easier.

Most physicians in New York say the hardest part of securing coverage isn’t the application - it’s understanding the differences between carriers, limits, tail obligations, and how venue severity affects pricing. The New York market is layered, and small details can change what you pay by a wide margin.

If you’d like a clearer sense of where you stand, DrsCoverage can gather quotes from the carriers writing in your county and walk you through the differences in plain language. You’ll see:

Physicians usually find that reviewing this side-by-side makes the entire process feel much more manageable - especially when comparing admitted carriers with E&S options or navigating Section 18.

You can schedule a consultation with a licensed broker or request quotes whenever you’re ready. If you have a recent application or renewal packet, feel free to send it over - it usually helps us get initial indications more quickly. A DrsCoverage broker is available to help at any point in the process.

(3).svg)